Share-class hedging may not offer best-in-class hedging

There are two key features of currency exposure.

The first is that, depending on the volatility of the asset class, currency risk can meaningfully impact overall portfolio returns. The second is that currency exposure stemming from international assets is

expected to generate zero returns.

As such, managing currency risk can both reduce the volatility of an international portfolio as well as improve overall returns.

When gaining exposure to international assets via publicly traded funds, a common way to manage currency risk is to subscribe to the currency-hedged share class of a fund. Although this may seem an efficient and cost-effective option, our analysis shows that hedged share classes are often neither.

There are many hidden costs that can be incurred by managing currency for an international portfolio via a currency-hedged share class. Here are the key challenges we have identified:

Currency-hedged share classes are not always available

Sometimes asset managers do not provide a hedged share class for certain funds, typically due to limited investor demand or capacity constraints. This leaves many investors without a choice and therefore opting for the non-hedged share class. This is particularly true for funds investing in international illiquid assets. A dedicated currency manager can work to manage all currency exposure, regardless of the portfolio composition and its liquidity.

Currency-hedged share classes are often inefficient

1. Hedged share classes often only hedge the US dollar (USD) risk in the portfolio and leave other, smaller currency risks unmanaged. This leaves investors with a residual currency risk that can be significant, depending on the allocation of assets and the volatility of the unmanaged currency component.

If investors hold several funds with international asset exposures, holding several hedged share classes can lead to implementation inefficiencies and higher transaction costs. This is because the investors would not benefit from any netting across different currency exposure positions. This is particularly so if the assets in the funds have a low, or negative, correlation.

2. Currency risk is typically managed using derivatives, such as FX forwards, which require periodic funding of profits and losses at regular settlement intervals. An equity manager would need to maintain a cash buffer to meet any losses that arise, which leads to a structural reduction in exposure to the underlying equity index.

This has two direct implications: firstly, cashflows or collateral requirements managed at the individual investment level are not optimal and create additional drag; secondly, the fund manager of the hedged share class would be consistently under-investing in the underlying asset in order to maintain appropriate cash buffers for the FX hedges.

In our view, a significant benefit of using a dedicated currency manager is that they can be responsible for managing all currency risk at the overall portfolio level, after working out the net currency exposures from the full underlying list of international asset exposures. This type of approach should be expected to lead to more comprehensive and efficient currency hedging as well as more efficient management of the collateral pool.

The overall fees charged by currency-hedged share classes can be high and not transparent

A currency-hedged share class can be both expensive and opaque. Indeed, we have observed that these types of structures can charge 1bp to 2bp more than currency managers typically charge. Furthermore, as neither management fees nor trading costs are clearly monitored, there is a notable risk of non-competitive trading costs. Our experience is that a dedicated currency manager can offer transparency and achieve lower transaction

costs through curated trading relationships when compared to fund structures.

Currency-hedged share classes can often experience significant performance drag relative to their benchmarks

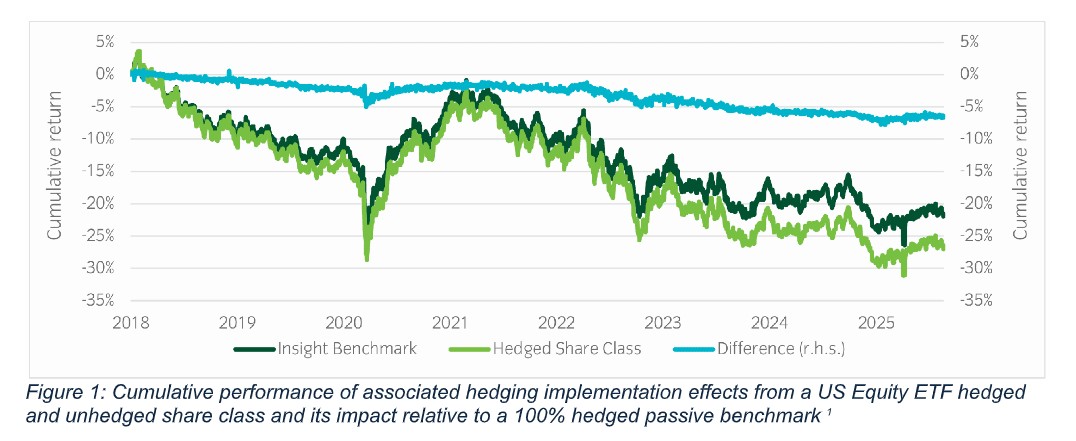

To demonstrate these hidden costs, we analyse a simple US Equity fund (an exchange-traded fund, or ETF), which has an AUD (unhedged) and an AUD hedged share class.

Considerable care has been taken to select a fund for which we can reasonably isolate the differences in observed returns from currency hedging. However, as we will illustrate below, there may be other additional factors which are not visible or fully transparent to investors allocating to share classes.

Figure 1 below shows the impact of passively hedging USD back to AUD – the ‘Insight Benchmark’. This assumes hedging using one month forwards with no management fees, adjusted for a conservative 10 per cent cash collateral pool with a 0 per cent yield alongside transaction costs in line with our historical execution. The ‘Hedged Share Class’ line shows the actual difference in historical returns between the unhedged share class and the hedged share class of the fund.

The fluctuation in both lines primarily reflects the impact of hedging the underlying USD risk of the assets.

However, the difference between the two shows there has been persistent underperformance from share-class currency hedging relative to a standard passive approach. In the example, between January 2018 and August 2025, the performance drag was approximately 87bps per annum above what could have been achieved by passive

currency hedging by a currency manager.

So, an investor who outsourced currency hedging at the fund level may have experienced additional performance drag relative to the benchmark, which was material and potentially unexpected, as the mechanics of a currency-hedged share class are largely invisible.

This performance drag could be due to additional management fees associated with currency hedging, bid-offer execution costs, and/or a relatively mechanistic currency- hedging approach employed by many passive managers with patterns known across the market (and potentially easy to anticipate). In the arena of passive investments, it is particularly ironic to note how much focus is given to tracking error, yet how silent nearly all parties are regarding the comparatively large frictional costs of currency-hedged share classes.

Conclusion

Investing in currency-hedged share classes to manage currency risk stemming from international investments may seem efficient and cost-effective, but our analysis shows that this may not be the case. As can be seen above, the ‘hidden costs’ of a hedged share class can be as high as 87bp per annum.

We believe a better approach to currency risk is to employ a specialist currency manager; one that can implement a bespoke currency program which will be more effective and cost efficient and will provide the investor full transparency on all costs.

Francesca Fornasari is head of currency solutions at Insight Investment.

Recommended for you

As the industry shifts from client-centric to consumer-centric portfolios, this personalisation is likely to align portfolios with investors’ goals, increasingly reflect their life preferences, and serve as a gateway to rewards and benefits.

In today’s evolving financial landscape, advisers are under increasing pressure to deliver more value to clients, to be faster, smarter, and with greater consistency.

Winning one premiership can come down to talent, luck, or timing but winning multiple ones indicates something deeper and successful is at play, writes Darren Steinhardt.

As fixed income markets evolve, advisers are questioning how to deliver consistent income, manage downside risk, and diversify exposures, all while navigating an uncertain interest rate environment