Is it time to currency hedge your portfolio?

The US dollar has been making headlines in 2025, caught up in the Trump Administration’s efforts to restructure the global economy through tariffs and other trade barriers, emphasising the importance of currency hedging.

Currency hedging is becoming increasingly important for Australian investors, particularly given the US dollar’s dominance in global markets. Over the past 10 years, the difference between being hedged or unhedged when investing in US assets amounted to a 62 per cent difference in total returns – a difference too large to ignore.

As a result, investors should pay close attention to movements in the greenback and their decision to, or not to, currency hedge.

What’s driving the AUD/USD?

The value of the AUD relative to other global currencies tends to be driven by:

- Interest rate differentials

- Global growth and associated demand for Australian commodities, and

- Risk sentiment.

Due to differing growth and inflation dynamics between Australia and the US, the AUD resumed a decade long downtrend in early 2021 dipping as low as US60c.

The interest rate differential between Australia and the US has inverted (i.e. the RBA cash rate is currently lower than the US Fed Funds rate) following the more extreme monetary response required by the US Fed to manage inflation in 2022.

The USD has also been supported in recent years by higher inflation and real yields in the US, a higher US terms of trade (i.e. a higher amount of exports relative to imports), higher economic growth in the US and the US' recent emergence as a net exporter of energy.

Then of course, the economic malaise in China has reinforced the US's role as the primary engine of global growth, weighing on commodity sensitive currencies such as the Australian dollar.

In 2024, the US outperformed relative to other major economies, and that bullish sentiment was reinforced by Trump’s “America First” rhetoric upon returning to the Presidency. Global investors scrambled for US stocks and bonds, which appeared to offer higher returns and greater safety, driving the USD higher in the process.

Higher tariffs and broader trade uncertainty also initially strengthened the “safe haven” US dollar whilst more “cyclical” currencies like the AUD weakened.

While these factors saw the AUD/USD fall to 20-year lows there are early signs of these trends reversing and the USD running out of steam.

Why the AUD could strengthen

Currently, the scope for continued USD strength looks increasingly limited.

Positioning in the greenback appears elevated, and on most fundamental currency metrics like purchasing power parity, the USD is considered overvalued.

A persistently strong US dollar also conflicts with the trade goals of the Trump Administration - namely to reduce the US’ trade deficit with major trading partners, such as China and Europe, in a bid to revitalise domestic industries and create domestic jobs under an “America First” populist agenda.

Meanwhile, the AUD could receive support if the Chinese government rolls out expansionary stimulus in a bid to counter the impact of US tariffs and to restore policy credibility and market confidence which may improve risk sentiment and support commodity prices.

These developments could catalyse a dramatic mean reversion in the Aussie dollar which is currently 13 per cent below its long-term average (around US$0.75 to 30 April 2025) at time of writing. This would have significant impacts on Australian investor returns at a time when they are more exposed to the USD than ever.

The case for tactical currency hedging

Most global equities and global equity ETFs held by Australian investors are unhedged. In addition, self-directed investors tend to hedge significantly less than professionally managed model portfolios or superannuation funds, where hedge ratios are typically closer to 50 per cent (as reflected in APRA’s Simple Reference Portfolio benchmark).

This “under hedging” is occurring despite US equities, and by extension the US dollar, now comprising over 70 per cent of developed market benchmarks such as the MSCI World Index, still around the highest levels on record.

With US equities comprising most of the global benchmark, movements in the AUD/USD exchange rate have a major impact on unhedged returns. Over the past decade, being unhedged has provided a tailwind, but this dynamic can reverse – and there are clear historical precedents for extended AUD strength and relatively poor unhedged US and global equity returns.

Since the Australian dollar was floated in 1983, the AUD/USD has averaged around 0.75, and even in the past decade has touched 0.80 on multiple occasions.

Considering a long-term approach to currency hedging

Notwithstanding the points above, forecasting the direction, magnitude and timing of currency movements is very hard to get right. Even for investors who may not hold a strong view on currency movements, it’s also worth asking about the utility of hedging global equities.

In short, there are pros and cons to either approach. Based on Betashares analysis of historic data, there could be a case for currency hedging a portion of a portfolio’s global equities exposure from a return and volatility perspective.

For Australian investors, leaving a portion of your global equities exposure unhedged can lower portfolio volatility and drawdowns in periods of strong equity market drawdowns. This is because the AUD is seen as a “risk on” currency, whereas the US dollar is often regarded as “safe haven” currency which historically has tended to appreciate in periods of market sell-offs.

Trend can be your friend, or foe

If remaining unhedged or having a lower level of currency hedging is better from a drawdown and risk standpoint, what about portfolio returns?

Over a 35-year return period, the Australian dollar started and finished around US70c, and as a result the historic portfolio returns at all levels of currency hedging were approximately the same.

However, within this multi decade period, there were a number of 5-to-10-year periods where the AUD/USD trended strongly, both higher and lower.

For example, the AUD rallied significantly from US$0.50 in December 2001 to nearly US$0.90 in December 2007.

Over that time period, the S&P 500 Index returned 42 per cent in USD terms, but if an Australian investor held the S&P 500 Index unhedged, their return would have been -17 per cent in AUD terms.

This illustrates the potential implications of currency movements on portfolios – a point often forgotten, given the last decade has witnessed twin tailwinds of strong global equity performance and a weakening AUD.

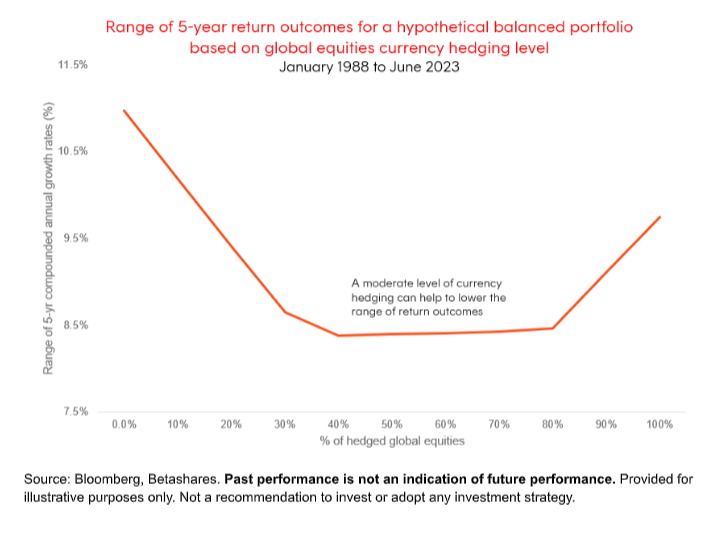

As part of some portfolio analysis, Betashares considered the return implications of currency hedging over different 5 year-time frames going back to 1988, where AUD appreciation or depreciation could have had a significant impact on overall outcomes for a hypothetical diversified portfolio.

The chart below shows the range of 5-year total return outcomes over the period 1988 – 2023 as a result of using different percentages of currency hedging for the global equity allocation (between 0 and 100 per cent hedged).

The range of return outcomes indicates the degree to which currency could impact investor outcomes (both negatively and positively). If an investor’s objective is to lower the impact of currency on long-term returns, they could consider an investment strategy with a lower outcome range.

Historically, the analysis found that being completely unhedged or 100 per cent hedged increased the return outcome uncertainty. Where the level of currency hedging employed was between 30 per cent – 80 per cent, there was far lower variability between the minimum and maximum 5-year return outcomes.

So, to hedge or not to hedge?

Investors with a view that the AUD is set to appreciate as the USD undergoes a fundamental challenge to its decade long dominance can choose to express a tactical view by increasing the hedged portion of their global equities portfolio.

For those not wishing to express a tactical view on currency, the analysis suggests an approach of currency hedging a portion of a global equities allocation could reduce the variability of long-term return outcomes making hedging still worthwhile.

As markets embrace more currency volatility under greater geopolitical and policy uncertainty, it is important for individual investors and their advisers to determine the level of currency hedging most suited to their own risk tolerance and objectives.

Ultimately, an investor should review their current hedge ratio and ask whether they are positioned for a potential rebound in the AUD.

Tom Wickenden is investment strategist at Betashares.

Recommended for you

As the industry shifts from client-centric to consumer-centric portfolios, this personalisation is likely to align portfolios with investors’ goals, increasingly reflect their life preferences, and serve as a gateway to rewards and benefits.

Managing currency risk in an international portfolio can both reduce the volatility, as well as improve overall returns, but needs to be navigated carefully.

In today’s evolving financial landscape, advisers are under increasing pressure to deliver more value to clients, to be faster, smarter, and with greater consistency.

Winning one premiership can come down to talent, luck, or timing but winning multiple ones indicates something deeper and successful is at play, writes Darren Steinhardt.