Central banks’ push for cheaper money raises key question

As central banks either look to act on cutting interest rates – including a second cut in as many months from our own Reserve Bank – the prospect of cheaper money has seen equities stocks rise and bond yields do the reverse, raising the question at JP Morgan’s market outlook this week of which market is pointing in the right direction.

Data from FE Analytics could provide some admittedly backwards-looking guidance. Looking at fixed interest – global bonds sector, the funds to offer the best returns in light of the overall slump in the last month – where the sector returned 1.01 per cent on average – were focused on emerging markets. The Colchester Emerging Markets Bond fund (returning 4.21 per cent for the month to 11 July), Mercer Emerging Markets Debt fund (3.59 per cent) and PIMCO Emerging Markets Bond fund (3.04 per cent) were three of four retail funds to return over three per cent for the time period.

While emerging markets aren’t necessarily where investors look for fixed income options, these results reflected a broader conversation about the appeal of emerging market debt that is currently gaining traction.

Over the three months to 11 July, during which moves toward rate cuts were growing stronger, the Colchester and Mercer options above were again the best performers, returning 5.66 and 5.44 per cent respectively. American bonds also performed well – somewhat surprisingly in light of the Fed’s regular suggestions that a rate cut was imminent – with the Legg Mason Brandywine Global Income Optimiser X fund, which holds around 63.45 per cent of its funds in North America, and the CFS US Select High Yield fund being the only other two to return over five per cent for the period.

It's also worth noting that while on the face of it, global bond yields aren’t plummeting too strongly – FE Analytics reveals that their recent returns are fairly in-line with long-term performance – it’s a sector geared toward longer-term investors and some may be biding their time until central banks act more strongly, so the impact of current forecast for a drop in performance isn’t yet evident.

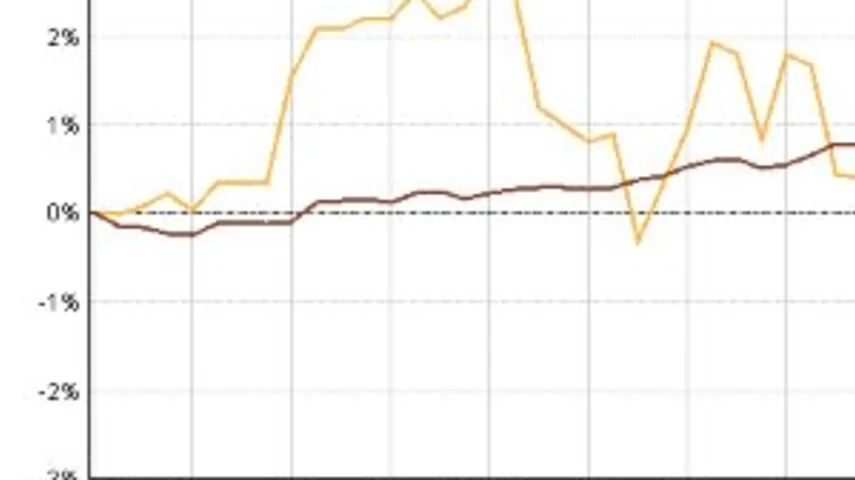

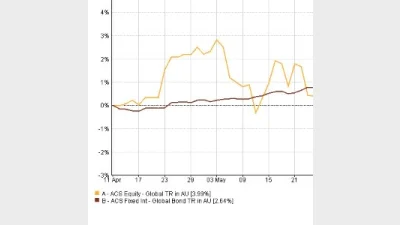

At the other end of the scales, global equity funds showed a significant leap in performance over the last month, as murmuring from central banks around cheaper money grew. Over the month to 11 July, almost 91 per cent of funds in the global equities sector outperformed the sector average of 1.93 per cent, compared to the 55 – 60 per cent that did over three and six-month and one-year periods.

Australia, having already received two interest rate cuts while other central banks are more hinting at them, could provide some guidance on what to expect globally. While just three funds in the global equities sector returned over 10 per cent in the last three months, for example, 12 Aussie equities funds hit double figures.

Performance was also strong over the last month, covering the period just after the first rate cut and including the second. The top performing fund over the time period, the Crescent Wealth Australian Equity Retail fund, returned 12.52 per cent. This is interesting in light of the Reserve Bank’s hope that the rate cuts will stimulate spending – almost a quarter of its funds are invested in consumer products. Further, its one-year performance to 11 July was just 1.09 per cent, suggesting that retail stocks have picked up since the cuts.

Speaking on the central banks’ activities’ impact on the market, JP Morgan Asset Management’s global market strategist, Kerry Craig, said: “Policy makers are no longer leaning against the door to easier monetary policy, its wide open and they are dusting off the welcome mat.

“But it is no longer just the case of lowering rates to boost economic activity, as many central banks have been unable to normalise interest rates and have less scope to ease. In the case of the Fed, it’s whether the committee really can stop at just two cuts. A longer cycle of cuts comes with unfriendly market connotations.”

The chart below shows the performance of both the global equities and global bonds sectors over the last three months.

AUTHOR

Hannah Wootton

Recommended for you

Clime Investment Management has sold a portion of its retail client book to an external financial planning practice for $1.6 million in its latest cost-out move.

In his inaugural address as L1 Group chief executive, Julian Russell has outlined his vision and priorities for the newly-merged $16.7 billion business but warned fund outflows will continue for 18 months.

Ten Cap has announced it will launch its first active ETF on the ASX later this month, expanding retail access to its flagship Australian equities strategy.

Flows into cash and fixed income ETFs rose by 46 per cent in October with investors particularly demonstrating a preference for Australian credit ETFs as they move away from AT1 bank hybrids.