Superannuation death benefits explained

It is vital that superannuation fund members have an understanding of death benefits, says ING Australia's Scott Quinn.

With Australian social trends of increasing de facto relationships and blended families, it is important that superannuation fund members are aware of what will happen to their superannuation benefits upon their death.

“That’s easy,” I hear you say. “Simply nominate a beneficiary for the superannuation fund”.

Unfortunately, these could be your famous last words. In many cases it’s not that simple.

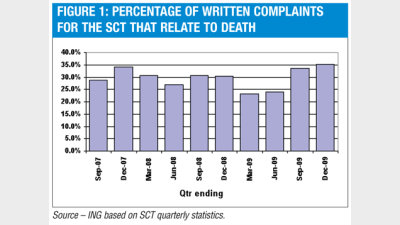

Each year approximately one in three complaints falling within the jurisdiction of the Superannuation Complaints Tribunal (SCT) relate to death. These include cases where beneficiaries were nominated for the superannuation fund.

Typically, complaints lodged with the SCT are based on one or more of the following arguments:

- that the distribution of the death benefit is not fair and reasonable;

- that the nominated beneficiary does not satisfy the definition of a dependant;

- that the member did not have the capacity to understand the decision they were making when they made the nomination; and

- that the correct procedures were not followed when establishing a traditional (lapsing) binding nomination.

The following determination (D07-08\030) was made by the SCT in 2007 where a binding nomination was determined to be invalid because it was ambiguous.

SCT Determination One

The sister of the deceased member, acting in her capacity as enduring power of attorney at that time, effected a binding death benefit nomination nominating two estranged children of the deceased to each receive 37.5 per cent and her to receive 25 per cent. This reflected the distribution of assets via the Will.

Upon the death of the member, the trustee decided that the binding death benefit nomination was valid, but the 25 per cent paid to the sister was in her capacity as the legal personal representative of the deceased.

The trustee concluded that the sister was not a dependant of the deceased therefore she must have nominated herself as the legal personal representative.

The SCT determined that the nomination was ambiguous. In accordance with the Trust Deed, the trustee should have disregarded the nomination and paid the entire death benefit to the estate.

A valid binding death benefit nomination can ensure that the death benefits are paid in accordance with the member’s wishes.

However, the validity of the binding death benefit nomination may be scrutinised. A good understanding of superannuation death benefits, the death benefit process of the superannuation fund and a contingency plan addressing the superannuation benefits within the Will is the best way to mitigate this risk.

If the death benefit is paid to the estate, it may become available to creditors of the estate and the estate could be contested. If contested, it is possible that the costs involved (which are commonly borne by the estate) are more detrimental to the beneficiaries than the reallocation of assets.

In the absence of a valid binding death benefit nomination, some trustees may have discretion to determine how to distribute the death benefits. Any discretionary decision made by the trustee may be contested.

An SCT determination (D08-09\063) handed down in 2009 illustrates how different the death benefit distribution can be if it was paid in accordance with the:

- Nomination made by the member;

- Trustee decision; or

- SCT determination.

SCT Determination Two

At the time of death, the deceased provided financial assistance to his girlfriend (they had a long-term relationship but didn’t reside together), his spouse (separated), his daughter and his mother. All qualified as dependants.

The deceased had completed a non-binding nomination nominating:

- 25 per cent to his spouse;

- 50 per cent to his daughter; and

- 25 per cent to his mother.

Since this nomination was non-binding, the superannuation fund trustee decided to pay:

- 25 per cent to the spouse;

- 59 per cent to the daughter;

- 11 per cent to the mother; and

- 5 per cent to the girlfriend.

The trustee was informed that the mother had died before making their final decision; however the trustee argued that the mother was alive at the time of making their preliminary decision and her subsequent death was irrelevant.

The SCT set aside the decision made by the trustee and determined that the death benefit should be distributed:

- 52 per cent to the spouse;

- 26 per cent to the daughter; and

- 22 per cent to the girlfriend.

The SCT determined that the mother should not receive any part of the distribution, because she died prior to the final determination and any payment to her estate would not satisfy the requirement for the superannuation death benefit to be paid to the member’s dependants (beneficiaries of the mother’s estate were not dependants of the deceased member).

Unlike the member and the trustee who both weighted the distribution heavily in the daughter’s favour, the SCT heavily weighted the distribution towards the spouse.

The SCT determined that this was fair and reasonable based on the current level of support provided to each and the expected level of future support. The daughter unsuccessfully appealed the decision in the Federal Court.

Where the distribution of a death benefit is contested, the reallocation of the death benefits is not the only problem. Contesting the decision can also cause considerable delays in determining who is ultimately entitled to the death benefit.

SCT Determination One took two years from the date of death to the final determination. SCT Determination Two took three years.

Conclusion

When it comes to the direction of superannuation death benefits, binding nominations (lapsing and non-lapsing) certainly have an advantage over non-binding nominations. However, care should be taken to ensure that the binding nomination is valid.

A good understanding of superannuation death benefits and the death benefit process of the superannuation fund is the key to achieving the desired outcome.

Whether from a blended family or not, disputes often arise over the distribution of death benefits. Adequately dealing with the distribution of superannuation death benefits, in conjunction with the estate of the deceased, can avoid family conflict and lengthy delays.

As Francis Edward Smedley wrote, “all’s fair in love and war” — particularly where death benefits are dealt with inadequately.

Scott Quinn is technical services manager at ING Australia.

Recommended for you

When entering paid employment, it’s not long before we are told that we’ll need to lodge a tax return but there are times when a person will be excepted.

Anna Mirzoyan examines how grandfathering affects income support payments and how factors such as paying for aged care can impact them.

There are specific requirements that only apply to trustees of self-managed superannuation funds, writes Tim Howard, including the allocation in their investment strategy.

Investments bonds offer a number of flexible, tax-advantaged benefits, writes Emma Sakellaris, but these are often overlooked as old fashioned when it comes to portfolio allocations.